Clarity for First-Time Buyers: The Houston Homebuying Checklist including Frequently Asked Questions

Buying your first home in Houston is exciting. It’s also, let’s be honest, a little overwhelming. Between mortgage applications, home inspections, title companies, and Houston’s unique flood disclosure requirements, there is a lot to track.

That’s exactly why this checklist exists. Whether you’re 12 months away from buying or ready to make an offer next month, this guide gives you every step — in the right order — so nothing falls through the cracks.

Bookmark this page. Print the checklist. OR CLICK HERE for your own interactive electronic checklist. Share it with your partner. And follow it step by step. First-time buyers who have a clear plan consistently have better outcomes than those who don’t.

✅ WHAT THIS GUIDE COVERS: Finances & credit • Mortgage pre-approval • Houston home search • Making an offer • Inspections & appraisal • Closing • Move-in essentials

PHASE 1 — 3 TO 12 MONTHS BEFORE BUYING

Step 1: Get Your Finances and Credit Ready

Before you talk to a lender, talk to your money. Your financial health determines how much house you can afford, what interest rate you’ll qualify for, and how strong your offer will look to sellers. Most first-time buyers in Houston need 3–12 months to get their finances in shape — the sooner you start, the better your options.

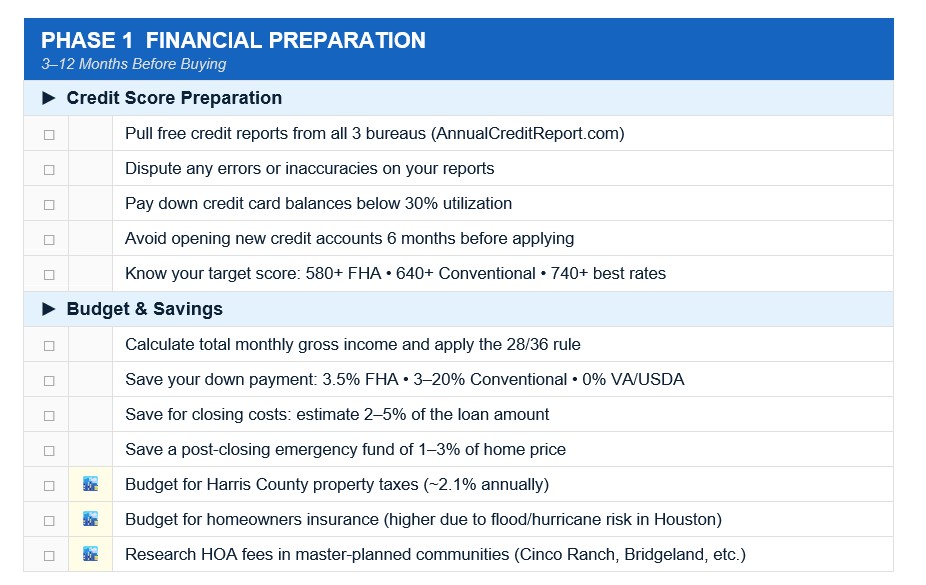

Your Credit Score Checklist

- Pull your free credit reports from all three bureaus at AnnualCreditReport.com

- Dispute any errors or inaccuracies you find — these can drag down your score unnecessarily

- Pay down credit card balances to below 30% of each card’s limit

- Avoid opening any new credit accounts in the 6 months before applying for a mortgage

- Avoid closing old accounts, even ones you don’t use — they help your credit age

- Know your target: 620 minimum for FHA loans, 640+ for most conventional loans, 740+ for the best rates

Your Budget Checklist

- Calculate your total monthly gross income (before taxes)

- Apply the 28/36 rule: housing costs should not exceed 28% of gross income; all debt not exceed 36%

- Factor in ALL homeownership costs, not just the mortgage: property taxes (avg. 2.1% in Harris County), homeowners insurance, HOA fees, maintenance, and utilities

- Build your down payment savings goal: 3% (FHA minimum), 3.5% (FHA standard), 5–20% (conventional)

- Save a separate emergency fund of 1–3% of the home price for unexpected repairs after closing

- Account for closing costs: typically 2–5% of the loan amount ($6,000–$15,000+ on most Houston homes)

🏙️ HOUSTON SPECIFIC: Harris County property taxes average 2.09% annually — one of the highest rates in the country. A $350,000 home could carry $7,300+ per year in property taxes alone. Always factor this into your monthly budget.

PHASE 2 — 2 TO 4 MONTHS BEFORE BUYING

Step 2: Understand Your Houston Mortgage Options

Houston first-time buyers have access to several loan programs, including federal programs and Texas-specific assistance. Knowing your options before you talk to a lender puts you in a far stronger position.

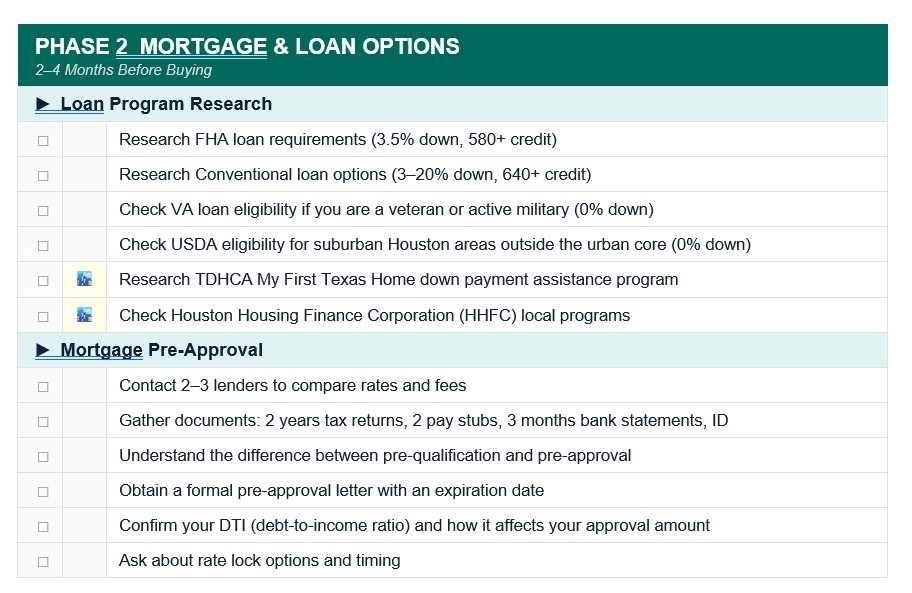

Loan Types to Research

- FHA Loan — 3.5% down, more flexible credit requirements (580+ score), requires mortgage insurance

- Conventional Loan — 3–20% down, no mortgage insurance above 20%, requires stronger credit (640+)

- VA Loan — 0% down for eligible veterans and active military, no mortgage insurance

- USDA Loan — 0% down for homes in eligible rural/suburban areas outside Houston’s urban core

- Texas Department of Housing and Community Affairs (TDHCA) — My First Texas Home program offers down payment assistance for qualifying buyers

- Houston Housing Finance Corporation (HHFC) — local programs for income-qualifying first-time buyers

Mortgage Pre-Approval Checklist

- Contact at least 2–3 lenders to compare rates and fees (this matters — rates vary by lender)

- Gather required documents: last 2 years of tax returns, last 2 pay stubs, last 3 months of bank statements, government-issued ID, and rental history if applicable

- Understand the difference between pre-qualification (estimate) and pre-approval (verified commitment)

- Get a formal pre-approval letter — this is required by most Houston sellers before reviewing offers

- Confirm how long your pre-approval is valid (typically 60–90 days) and plan your search timeline accordingly

- Ask your lender specifically about DTI (debt-to-income ratio) limits and how your current debts affect your approval amount

💡 PRO TIP: Getting pre-approved by multiple lenders within a 14–45 day window counts as only one hard credit inquiry. Shop aggressively — even a 0.25% difference in rate saves thousands over the life of a loan.

PHASE 3 — ACTIVE HOME SEARCH

Step 3: Hire a Houston Buyer’s Agent and Start Your Search

Your real estate agent is your most important partner in this process. A great Houston buyer’s agent is free to you (the seller pays the commission), knows the local market deeply, and protects your interests at every step.

Choosing Your Agent Checklist

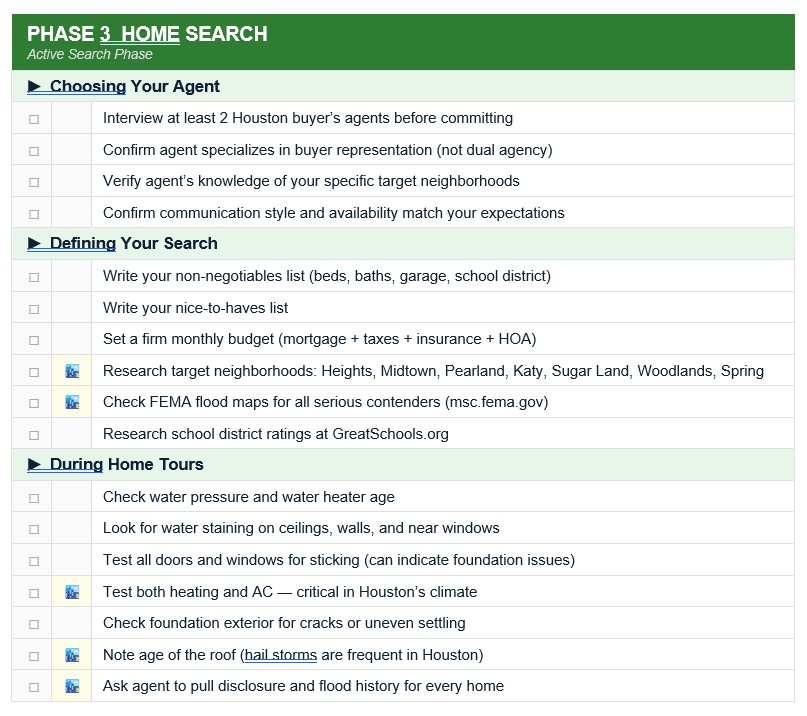

- Interview at least two agents before committing

- Ask specifically about their experience with first-time buyers

- Verify they know your target neighborhoods — Houston is hyperlocal; what’s true in The Heights is different from Katy

- Confirm they will represent only your interests (buyer’s agency, not dual agency)

- Ask how they communicate: are they available via text, how quickly do they respond to new listings?

Defining Your Search Criteria Checklist

- List your non-negotiables: bedrooms, bathrooms, garage, school district

- List your nice-to-haves: backyard size, updated kitchen, commute distance

- Set a firm maximum budget — include taxes and insurance in your monthly calculation, not just the mortgage

- Research target Houston neighborhoods: The Heights, Midtown, Pearland, Katy, Sugar Land, The Woodlands, Spring, Humble, and others

- Check FEMA flood maps for any home you’re serious about — flood zone designation affects insurance cost significantly

- Research school district ratings at GreatSchools.org even if you don’t have children — it affects resale value

During Home Tours Checklist

- Check water pressure and water heater age in every home

- Look for signs of water staining on ceilings, walls, and near windows

- Open every door and window — sticking frames can indicate foundation movement

- Test HVAC by running both heat and AC — Houston’s climate demands a reliable system

- Check the foundation around the exterior for cracks or uneven settling

- Ask your agent to pull the property’s disclosure and flood history

- Note the age of the roof — Houston’s hail storms shorten roof lifespans

🏙️ HOUSTON SPECIFIC: Always check whether a home is in a flood zone before making an offer. Search the address on FEMA’s Flood Map Service Center (msc.fema.gov). Flood insurance in high-risk zones can add $1,500–$4,000+ per year to your housing costs.

PHASE 4 — MAKING AN OFFER

Step 4: Make a Strong, Informed Offer

Making an offer is where preparation pays off. First-time buyers who have done their homework — and have an experienced agent guiding them — write stronger offers and win more negotiations.

Before You Make an Offer Checklist

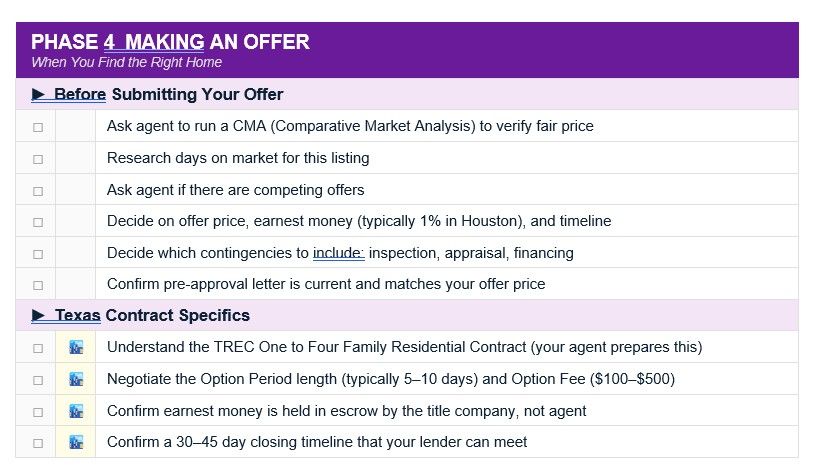

- Ask your agent to run a Comparative Market Analysis (CMA) to confirm the home is priced fairly

- Research how long the home has been on the market — longer days on market = more negotiating leverage

- Ask if there are other offers (your agent should ask the listing agent)

- Decide on your offer price, earnest money amount (typically 1% of purchase price in Houston), and closing timeline

- Decide whether to include contingencies: home inspection, appraisal, financing, and/or home sale

- Confirm your pre-approval letter is current and matches your offer amount

Texas-Specific Offer Details

- Texas uses the TREC One to Four Family Residential Contract — your agent will prepare this

- Option period: Texas contracts include an Option Period (typically 5–10 days) during which you pay an Option Fee and can terminate for any reason

- Earnest money: typically held in escrow by the title company, not the seller’s agent

- Closing timeline: 30–45 days is standard in Houston; ask your lender to confirm they can meet the date

💡 PRO TIP: The Option Period in Texas is your most powerful protection as a buyer. During this window you can hire inspectors, review disclosures, and walk away for any reason — losing only your Option Fee (typically $100–$500). Use it wisely.

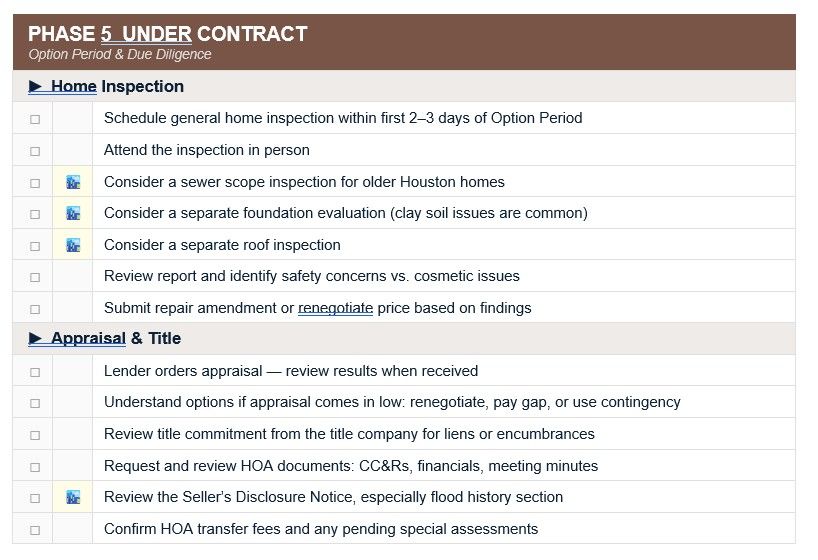

PHASE 5 — UNDER CONTRACT

Step 5: Navigate Inspections, Appraisal, and Due Diligence

Once your offer is accepted and you’re under contract, the clock starts on your Option Period and due diligence phase. This is one of the most important phases of the entire process — and one of the most time-sensitive.

Home Inspection Checklist

- Schedule your general home inspection within the first 2–3 days of the Option Period

- Attend the inspection in person whenever possible — you’ll learn more about the home in 3 hours than in 10 tours

- For Houston homes, also consider: a sewer scope inspection, a foundation evaluation (especially for older homes), and a separate roof inspection

- Review the inspection report carefully and identify items that are safety concerns vs. cosmetic issues

- Work with your agent to submit a repair amendment requesting seller remediation or a price reduction for significant issues

- Understand your options: request repairs, request a credit at closing, reduce the offer price, or walk away

Appraisal Checklist

- Your lender will order a professional appraisal to confirm the home’s value supports the loan amount

- If the appraisal comes in lower than your offer price, you have several options: renegotiate the price, pay the difference in cash, or use your appraisal contingency to walk away

- In Texas, the appraisal contingency is separate from the financing contingency — confirm both are in your contract if needed

Title and HOA Due Diligence

- Review the title commitment sent by the title company — look for any liens, easements, or encumbrances on the property

- If the home is in an HOA, request and review the HOA documents: CC&Rs, bylaws, financial statements, and meeting minutes

- In Texas, sellers are required to provide HOA documents; you have a 3-day right of rescission after receiving them

- Confirm the HOA’s monthly fee, special assessments pending, and any transfer fees

🏙️ HOUSTON SPECIFIC: Texas law (Chapter 5 of the Texas Property Code) requires sellers to provide a Seller’s Disclosure Notice covering known defects, flood history, and other material facts. Review this disclosure carefully with your agent — any known flood damage must be disclosed.

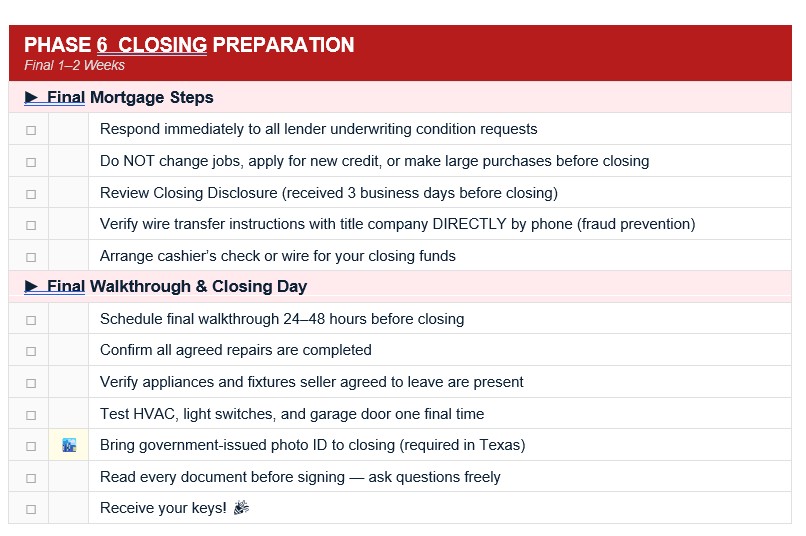

PHASE 6 — FINAL STEPS BEFORE CLOSING

Step 6: Prepare for Closing Day

The final 1–2 weeks before closing involve lender reviews, final walk-throughs, and logistical preparation. Stay responsive to your lender, don’t make any major financial moves, and keep your documents organized.

Final Mortgage and Lender Checklist

- Respond immediately to any lender requests for additional documents (underwriting conditions)

- Do NOT change jobs, apply for new credit, or make large purchases before closing — this can cause your loan to fall through

- Review your Closing Disclosure (you’ll receive it at least 3 business days before closing) and compare it to your Loan Estimate

- Confirm your wire transfer instructions with the title company DIRECTLY by phone — wire fraud is a real risk in real estate transactions

- Confirm the exact amount you need to bring to closing and arrange a cashier’s check or wire transfer

Pre-Closing Walkthrough Checklist

- Schedule your final walkthrough 24–48 hours before closing

- Confirm all agreed-upon repairs have been completed

- Verify that all appliances, fixtures, and systems the seller agreed to leave are still present and functioning

- Check that the property is in the same condition as when you made your offer

- Test light switches, garage doors, and HVAC one final time

Closing Day Checklist

- Bring a government-issued photo ID (required in Texas)

- Bring your cashier’s check or confirm wire transfer has been sent

- Read every document before signing — closing typically takes 1–2 hours

- Ask the title officer to explain anything you don’t understand — you have that right

- Receive your keys — you are now a homeowner!

PHASE 7 — AFTER CLOSING

Step 7: First-Time Homeowner Move-In Checklist

Closing day is the beginning, not the end. The first 30 days in your new Houston home are critical for setting up safety systems, transferring utilities, and protecting your investment.

First Week Priorities

- Change all exterior door locks and garage codes immediately

- Locate and label your main water shut-off valve, electrical panel, and gas shut-off

- Transfer utilities to your name: CenterPoint Energy (gas/electric), your internet provider, and the City of Houston for water if applicable

- Set up homeowners insurance if it wasn’t already in place at closing

- File for Homestead Exemption with HCAD (Harris County Appraisal District) — this reduces your taxable value by up to $100,000+ for school district taxes and must be filed by April 30th of the year following purchase

First Month Priorities

- Test every smoke detector and carbon monoxide alarm; replace batteries

- Locate the cleanout for your sewer line in case of future plumbing issues

- Schedule your first HVAC filter change and set a reminder every 30–90 days

- Introduce yourself to neighbors — they’re your best source of hyper-local information

- Document the condition of your home with photos and videos for insurance purposes

- Create a home maintenance calendar for seasonal tasks (gutter cleaning, HVAC service, etc.)

🏙️ HOUSTON SPECIFIC: The Homestead Exemption is one of the most valuable benefits of owning in Texas — but you must apply. File at hcad.org (Harris County) or your county’s appraisal district. A $300,000 home with a homestead exemption can save you $1,200–$1,500 per year in property taxes.

Frequently Asked Questions: First-Time Home Buyers in Houston

❓ How long does it take to buy a house in Houston as a first-time buyer?

From the time you start preparing your finances to closing day, the typical timeline for a first-time buyer in Houston is 3–6 months. The home search itself averages 4–8 weeks in most Houston submarkets, and closing takes 30–45 days once you’re under contract.

❓ What credit score do I need to buy a house in Houston?

You need a minimum of 580 to qualify for an FHA loan with a 3.5% down payment, or 500 with 10% down. For conventional loans, most lenders require 620–640. To get the best interest rates available, aim for a 740 or higher.

❓ How much do I need for a down payment in Houston?

It depends on your loan type. FHA loans require as little as 3.5% down. Conventional loans can go as low as 3% for qualifying buyers. VA and USDA loans require 0% down for eligible borrowers. Texas also has down payment assistance programs through TDHCA for qualifying first-time buyers.

❓ Do I need flood insurance for a home in Houston?

It depends on the home’s flood zone designation. If the home is in a FEMA Special Flood Hazard Area (SFHA), flood insurance is required by your lender. Even outside high-risk zones, flood insurance is strongly recommended in Greater Houston given the region’s history with major storm events.

❓ What is the Option Period in Texas?

The Option Period is a Texas-specific contract provision that gives buyers a set number of days (typically 5–10) to conduct due diligence and terminate the contract for any reason. You pay a small Option Fee (usually $100–$500) to the seller for this right. It’s one of the strongest buyer protections in the country.

❓ What is the Homestead Exemption and how do I get it in Houston?

The Homestead Exemption reduces the taxable value of your primary residence for property tax purposes. In Texas, it removes up to $100,000 from your home’s value for school district taxes and caps your annual appraisal increase at 10%. File with your county’s appraisal district (HCAD for Harris County) by April 30th of the year following your purchase. It’s free to apply.

❓ Should I use the same agent to buy and sell a home in Houston?

You can, but make sure that agent genuinely has bandwidth and expertise on both sides of the transaction. For most first-time buyers, the buying side is the priority — choose an agent who specializes in buyer representation and has deep knowledge of your target Houston neighborhoods.

You’re More Ready Than You Think

Buying your first home in Houston is one of the best financial decisions you can make. Houston offers genuine affordability, strong long-term appreciation in the right neighborhoods, and a dynamic economy that supports property values.

The homebuying process can feel complicated — but broken into phases with a clear checklist, it becomes manageable. Most first-time buyers say the biggest thing they wish they’d had was a clear plan from the beginning. Now you have one.

Use this checklist as your roadmap. Revisit it at each phase. Share it with anyone helping you through the process. And remember: you don’t have to figure this out alone.

📞 NEXT STEP: If you’re a first-time buyer planning to purchase in Houston, a free strategy consultation can help you assess where you are in the checklist and what to prioritize next. The earlier you plan, the more options you have.

Houston homebuying checklist • mortgage options Houston first-time buyer • Houston buyer’s agent checklist • making an offer on a home in Texas • home inspection checklist Houston • closing day checklist Texas • Houston homestead exemption • Houston flood zone home buying • first-time homeowner move-in checklist

Categories

Recent Posts